Λ3THER RESEARCH BRIEF

Echoes of 1999: Deconstructing The AI Rally's Fragile Foundation

June 03, 2026

The market's AI euphoria isn't a product of fundamental revolution, but a dangerous cocktail of historical echo, central bank liquidity, and a circular flow of capital that masks profound systemic risk.

EXECUTIVE THESIS // TACTICAL VIEW

The current AI-driven market rally is not a function of intrinsic value but a structural mirage built on three pillars: a speculative momentum that mirrors the 1999 dot-com bubble, a direct lifeline of central bank liquidity that has inflated all risk assets, and a self-referential capital loop where AI startups burn venture funding on hyperscaler infrastructure, creating the illusion of organic growth. This system is critically dependent on the continued availability of cheap capital. The primary trigger for a violent repricing is not a failure of AI technology itself, but a contraction in macro liquidity, which would expose the circular financing and break the feedback loop.

History rarely repeats, but its echoes can be deafening. The current market narrative, supercharged by the promise of Artificial Intelligence, has drawn countless comparisons to the dot-com boom of the late 1990s. While proponents argue today's rally is built on the real earnings of profitable tech giants—unlike the speculative IPOs of 1999—this view misses the structural similarities that lie beneath the surface. The psychological setup, the parabolic price action, and the belief in a "new paradigm" are rhyming with alarming precision. The key difference isn't the technology, but the source of the fuel. The dot-com bubble was inflated by retail euphoria and venture capital; today's AI boom is underwritten by the central banks of the world.

📈 Section 1: The Ghost of 1999

The big picture: The Nasdaq's ascent since 2023 bears an uncanny resemblance to its trajectory from 1997-2000. According to analysis from BTIG, the top 10 performing stocks in the Nasdaq 100 over the past year have surged an average of 784%, a figure that eclipses the 622% gain seen by the top performers in the year leading up to the March 2000 peak. This isn't just a rally; it's a momentum-driven vertical climb, characteristic of a speculative fever rather than a measured response to fundamental growth.

Why it matters: While today's leaders like Nvidia are immensely profitable, unlike the Pets.coms of the past, the market's valuation methods are becoming detached from reality. The Shiller price-to-earnings ratio for the U.S. market has exceeded 40 for the first time since the dot-com crash, and the S&P 500 is trading at 23 times forward earnings—the most stretched since that era. This suggests that even with real earnings, the expectations priced in are bordering on perfection, leaving no room for error or a slowdown in the breakneck growth. The chart below visualizes this parabolic phase, a pattern that historically resolves in sharp, painful corrections.

The bottom line: The debate over whether this is a bubble misses the point. The critical takeaway is that the market is exhibiting the *behavior* of a late-stage speculative rally. The concentration of returns in a few "picks and shovels" names, the extreme performance of the top 10 stocks, and the euphoric narrative are all classic warning signs. Whether backed by earnings or not, a market that moves this far, this fast, becomes inherently fragile. The question is not *if* the technology is real, but whether the valuations are sustainable. History suggests they are not.

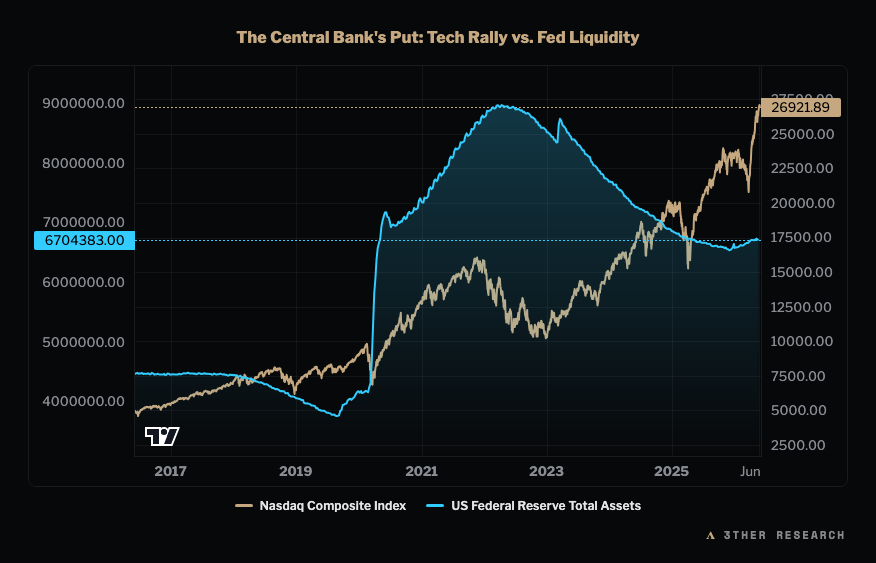

🏦 Section 2: The Macro Liquidity Lifeline

Zooming out: The engine of this AI-fueled rally is not superior code or breakthrough algorithms alone. It is, fundamentally, a story of macro liquidity. Since the 2008 financial crisis, and accelerated dramatically during the 2020 pandemic, the Federal Reserve's balance sheet has acted as a primary driver for risk asset valuations. The correlation is undeniable: as the Fed's assets expanded from under $1 trillion to nearly $9 trillion, the stock market, led by tech, followed in lockstep.

How it works: The mechanism, known as quantitative easing (QE), involves the central bank purchasing assets like Treasury bonds. This injects liquidity into the financial system and forces investors out of safe assets and into riskier ones, like tech stocks, in a search for yield. This has created an environment where cheap capital is abundant, fueling venture investment, stock buybacks, and speculative IPOs. The AI boom did not happen in a vacuum; it ignited in a world already saturated with central bank-provided capital. As of late 2025 and into 2026, many central banks have pivoted back to an accommodative stance, reinforcing this liquidity backstop.

Why it matters now: This direct link between the Fed's balance sheet and the Nasdaq makes the market exceptionally vulnerable to monetary policy shifts. The entire valuation structure of the AI ecosystem rests on the assumption of continued liquidity. Any serious attempt by the Fed to shrink its balance sheet (Quantitative Tightening) or a spike in inflation that forces a hawkish pivot could pull the rug out from under the market. The rally is not tethered to fundamentals in a vacuum; it is tethered to the availability of cheap money. As the chart above clearly shows, the market's trajectory has been heavily influenced by the expansion and contraction of the Fed's assets.

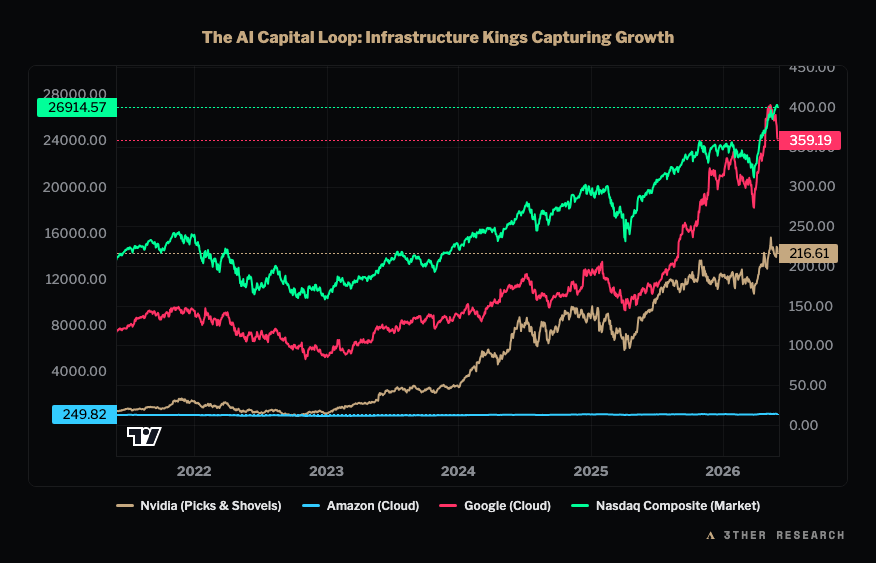

🔄 Section 3: The Great AI Capital Round-Trip

The inside story: Beyond the historical parallels and macro liquidity lies a more subtle and powerful dynamic: a circular flow of capital that creates a distorted picture of economic reality. This isn't a conspiracy; it's a closed-loop system where the biggest players are effectively paying themselves.

Here’s the mechanism in three steps:

- Step 1: Capital Injection. Hyperscalers like Microsoft, Amazon, and Google invest billions into promising AI startups like OpenAI and Anthropic, receiving equity in return.

- Step 2: Capex Burn. To train their massive models, these AI startups must spend the vast majority of that invested capital on cloud computing and specialized hardware (GPUs). They pay it right back to the cloud divisions of their investors (Azure, AWS, Google Cloud) and to the dominant chipmaker, Nvidia.

- Step 3: Revenue Recognition. The hyperscalers then book this spending as high-margin cloud revenue, which Wall Street cheers, justifying their own soaring valuations. Nvidia's data center revenue, which now accounts for over 92% of its total, has exploded, driven almost entirely by this infrastructure buildout.

The result: A self-fueling cycle. Venture capital and corporate investment flows into AI labs, which is immediately routed to the tech giants as revenue, which in turn boosts their stock prices and provides them with more capital to invest back into the AI labs. It's a perpetual motion machine for as long as outside capital keeps flowing in. One analysis shows that by 2027, OpenAI's projected infrastructure costs will exceed its projected revenue by 3.5 times, requiring continuous external funding to survive.

The bottom line: This circular flow makes it appear as if there is a massive, organic, and profitable demand for AI services. In reality, a significant portion of the "demand" is simply the recycling of investment capital. The "picks and shovels" providers—Nvidia and the cloud giants—are the primary beneficiaries, absorbing nearly all the capital poured into the system. This creates an illusion of a robust, diversified ecosystem when, in fact, it's a highly concentrated and interdependent one.

💥 Section 4: The IPO Endgame and The Unwind

What's next: The culmination of this cycle is the impending wave of massive AI IPOs, with SpaceX, Anthropic, and OpenAI leading the charge. These debuts are designed to offload the immense private valuations onto the public markets, providing an exit for early investors and a fresh injection of capital to keep the circular flow going. The sheer scale of these offerings is unprecedented, with strategists warning that fund managers may need to sell existing holdings just to make room.

The catch: Public markets demand a clear path to sustainable, profitable growth—something that is difficult to prove for many AI models whose costs currently dwarf their revenues. The recent warning from Morningstar, valuing SpaceX at less than half of its target IPO price, highlights the deep skepticism among fundamental analysts about the viability of these valuations once they are subject to public scrutiny.

The two triggers for an unwind are clear:

- A Macro Liquidity Shock: A hawkish turn from the Federal Reserve, driven by persistent inflation or financial instability, would be the most potent catalyst. By draining the system of cheap capital, it would starve the AI ecosystem of the fuel it needs to sustain the circular financing loop.

- A Micro-Fundamental Failure: A major AI IPO that fails to perform, or a leading company like Nvidia reporting a significant deceleration in data center growth, could shatter the narrative of infinite expansion. This would cause investors to question the entire capital recycling scheme and re-evaluate the terminal value of the entire sector.

The current structure is a marvel of financial engineering, but it is built on a fragile foundation. The echoes of 1999 are a warning not about the promise of technology, but about the perils of a market detached from the constraints of macro reality.

Λ3THER Research is an independent financial publisher. All reports are for educational purposes and involve risk. Please review our full Regulatory Disclosures & Risk Warnings.