REGULATORY DISCLOSURE

A3THER Research LLC (“A3THER”) is a financial publisher and research provider. A3THER is not registered as an investment adviser, commodity trading advisor, broker-dealer, or financial planner with the U.S. Securities and Exchange Commission (SEC), the Financial Industry Regulatory Authority (FINRA), or any state or foreign regulatory authority. No content published by A3THER constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information is not tailored to individual circumstances and does not take into account the unique financial situation, investment objectives, or risk tolerance of any recipient. Nothing contained herein establishes a fiduciary, advisory, or client relationship between the reader and A3THER.

INVESTMENT RISK WARNING

All financial markets involve substantial risk, including the complete loss of principal. Highly volatile asset classes—including equities, sovereign bonds, commodities, foreign exchange, and digital assets—can experience sharp fluctuations. The research, opinions, analyses, projections, and reports published by A3THER are for general educational, historical, and informational purposes only. Readers must conduct their own independent due diligence and consult with a licensed financial adviser, tax professional, and legal counsel before making any investment decisions. Under no circumstances shall A3THER, its members, officers, or contributors be liable for any direct, indirect, incidental, special, or consequential trading losses or damages incurred as a result of relying on any data, models, charts, analysis, or strategic reviews published herein.

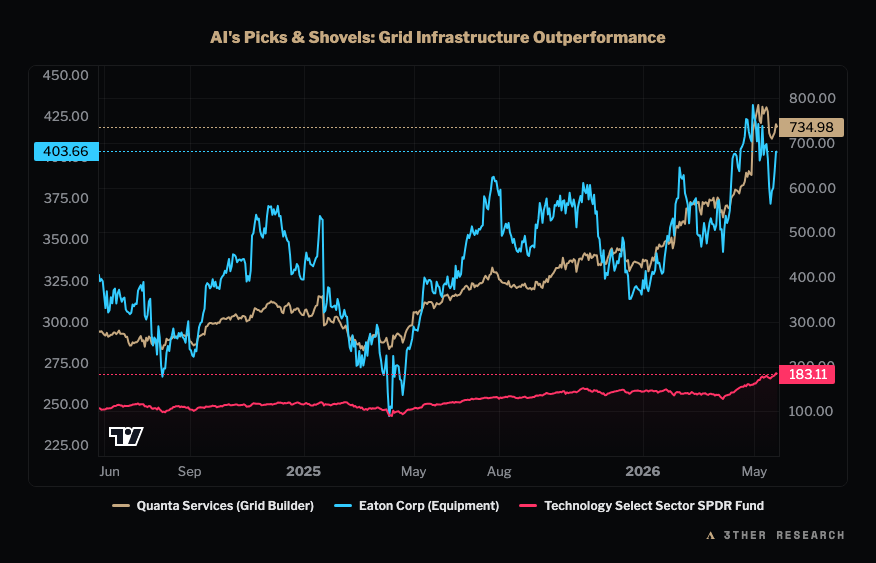

PROPRIETARY DATA & PROJECTIONS

Historical calculations, dual-axis charts, correlation matrices, and yield projections are synthesized using public APIs, scraping engines, and proprietary quantitative models. All charts and historical figures are for illustrative and conceptual purposes only. Hypothetical or backtested performance has inherent limitations, is not reflective of actual trading, and does not guarantee future results. Information is provided on an "as is" basis, without express or implied warranties of any kind regarding accuracy, completeness, timeliness, or reliability.

PRIVACY POLICY

At A3THER Research, we prioritize the privacy and security of our institutional clients and subscribers. We collect minimal personal data, restricted to registration emails and session preferences required to operate our analytical platform. Your email address is exclusively utilized for dispatching research updates and will never be shared, sold, or distributed to third parties. We leverage industry-standard cryptographic protocols to protect all stored information. If you wish to purge your subscription data or request details on collected metrics, please contact operations@a3ther.research.

TERMS OF SERVICE

By accessing the A3THER Research Portal or subscribing to our daily briefs, you agree to comply with and be bound by these Terms of Service. All content, analytical tools, models, and projections are the intellectual property of A3THER Research LLC and are licensed for personal, non-redistributable use. Redistribution, replication, or commercial exploitation of A3THER reports is strictly prohibited without prior written authorization. The services are provided "as is" and "as available" without warranties of any kind. We reserve the right to suspend subscription access or terminate user privileges at our discretion for violations of intellectual property guidelines.

FORM ADV PART II (SUMMARY)

By accessing the A3THER Research Portal, you acknowledge that A3THER Research LLC is not a registered investment adviser (RIA) and does not file a Form ADV with the SEC or state regulators. This portal provides research and publishing services exclusively. For entities requiring regulatory disclosure packets or operational due diligence (ODD) questionnaires, A3THER maintains an institutional fact sheet outlining its operations, data sources, and analytical methodologies. To request the institutional factsheet, please submit an inquiry through your family office or institutional representative to legal@a3ther.research.